Mortgage delinquency rates in Australia are starting to stabilise. MPA crunches the numbers to give you an idea of how the housing market is faring. Read on

After reaching decade-highs between 2018 and 2019, mortgage delinquency rates in Australia have begun to stabilise, the latest figures from S&P Global show. This reflects the resilience of the country’s property market.

The market intelligence firm’s residential mortgage-backed securities (RMBS) arrears statistics reveal very little change in Australian mortgage delinquency rates in the past few months. The figures remain low, which the company attributes to low unemployment levels and modest loan-to-value (LTV) ratio exposure.

To give mortgage professionals a picture of how the RMBS sector is doing, MPA crunches S&P’s performance index in this guide. We will provide a state-by-state breakdown of average mortgage delinquency rates from the past five years. We will also explain why arrears happen and what regulations are in place to protect both the borrowers and the lenders.

If you’re wondering about the health of the nation’s mortgage-lending sector, this article can help provide answers. Read on and learn more about mortgage delinquency rates in Australia and their impact on the overall housing market.

What is mortgage delinquency?

Mortgage delinquency happens when a borrower falls behind mortgage repayments for at least 30 days. This can be due to:

- personal hardships, such as marital disputes, illness, and death

- loss or reduction of income

- loan affordability resulting from interest-rate increases or other commitments

Banks and other lenders have a system in place to ensure borrowers meet strict lending criteria. A person’s circumstances, however, can change instantly. This can put them in a vulnerable position financially, hindering them from meeting monthly repayments.

Mortgage delinquency can have a negative impact on a person’s credit rating. If not addressed, it can also lead to the property’s foreclosure.

What is the average mortgage delinquency rate in Australia?

S&P’s February 2024 performance index (SPIN) shows that Australia’s mortgage delinquency rate is at 0.93%. This is a 2-basis-point dip in both monthly and year-on-year figures.

The data analytics firm has been collecting arrears statistics from the country’s RMBS sector since 1996. For this article, we will be comparing numbers over the past five years to get a picture of how the mortgage lending market was faring before, during, and after the pandemic.

We will present data on prime and non-conforming mortgages. For those new to the industry, prime mortgages are loans given to borrowers with good credit scores. Non-conforming home loans, on the other hand, are for borrowers with poor credit histories and unconventional needs.

Find out how aspiring homeowners can benefit from lenders mortgage insurance in this article.

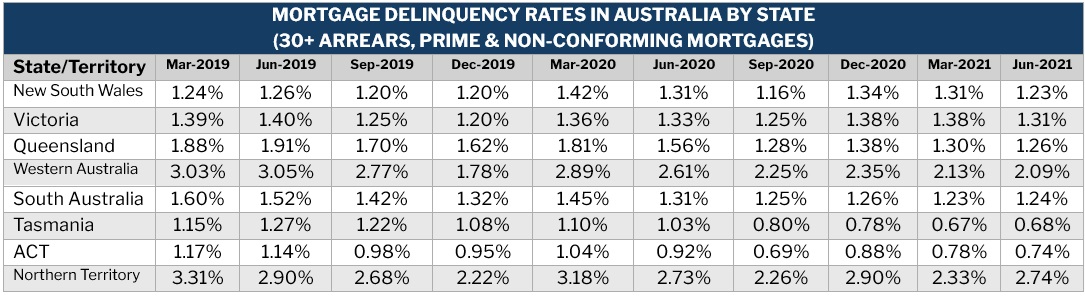

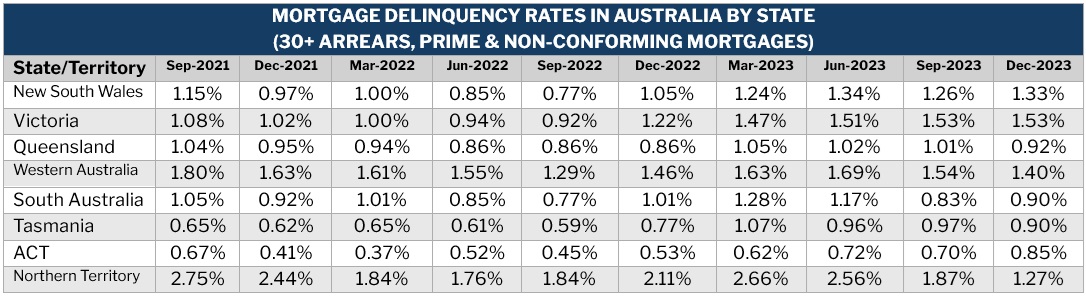

Here’s a quarterly summary of mortgage delinquency rates in Australia from March 2019 to December 2023. There are separate tables for non-conforming and prime mortgage arrears.

Mortgage delinquency rates Australia – prime mortgage, March 2019 to June 2021

Mortgage delinquency rates Australia – prime mortgage, September 2021 to December 2023

Mortgage delinquency rates Australia – non-conforming mortgage, March 2019 to June 2021

Mortgage delinquency rates Australia – non-conforming mortgage, September 2021 to December 2023

Here’s a state-by-state breakdown of mortgage delinquency rates in Australia during the same period. These are combined prime and non-conforming mortgage data for arrears of more than 30 days.

Mortgage delinquency rates Australia state-by-state breakdown, March 2019 to June 2021

Mortgage delinquency rates Australia state-by-state breakdown, March 2019 to June 2021

Mortgage delinquency rates Australia state-by-state breakdown, September 2021 to December 2023

What happens when a mortgage becomes delinquent?

Once a home loan becomes delinquent, lenders have two options:

- they can send a default notice on the day a mortgage repayment becomes overdue

- they can wait until the mortgage repayment is behind by 60 to 90 days or more before sending a notice

After receiving a default notice, borrowers have 30 days to meet all overdue payments. A mortgage default can be reflected on the borrower’s credit report if the repayments are behind by more than 60 days. But for this to happen, the lender must have sent the borrower these:

- written notice seeking repayment

- separate notice warning the borrower that the debt will be reported to a credit agency

The table below shows how the mortgage arrears process usually goes in Australia.

Mortgage delinquency rates Australia – how the default management process goes

|

Day 1 |

Day 30 to 60 |

Day 90 |

|

The lender contacts the borrower about the missed mortgage repayment.

The lender and the borrower make payment arrangements. |

The lender continues to contact the borrower.

The lender and the borrower discuss payment alternatives. These can include hardship arrangements. |

The lender starts the mortgage possession process, consisting of:

Legal action

Possession of property

Mortgage insurance

|

Mortgage arrears vs mortgage default: what’s the difference?

Mortgage arrears and mortgage default are often confused with each other, but there’s an important distinction between these industry terms.

Having a mortgage in arrears means that the borrower has fallen behind in payments. In Australia, banks and other lenders often offer a one- to two-week grace period for mortgage holders to settle a missed payment. If the loan is paid during this timeframe, it is still considered on time. If not, the borrower will be considered behind on their payments and classed by the lender as being in arrears.

After 60 days of being in arrears, the borrower can expect to receive a notice of default from the lender. This gives the mortgage holder 30 days to catch up with their repayments. Lenders are restricted by the law from offering a shorter notice period.

Lenders, however, can send a notice of default immediately after a missed payment, although they rarely do. Most lenders wait until the 90-day mark before acting.

Find out the 10 biggest mortgage lenders in Australia in our latest rankings.

Are there regulations governing residential mortgage-backed securities in Australia?

The National Credit Code (NCC) regulates most consumer credit transactions taking place in the country. It imposes a code of conduct on lenders. This includes licensing requirements, responsible lending practices, and providing consumers with comparison rates for mortgages and other loans.

The NCC is designed to ensure that borrowers are only approved for a loan that they can afford to pay. The code states that an unjust contract may be reassessed by a court in certain circumstances. These situations include a lender using unfair or dishonest tactics or failing to determine if a borrower can afford to meet loan repayments.

The NCC also contains hardship provisions such as a reduction in interest rates, lengthening of loan maturity, or full or partial deferral of interest for a temporary period. These concessions follow the Australian Prudential Regulation Authority’s (APRA) practice guidance for hardship loan arrears reporting. The guideline also states that missed payments will continue to accumulate until these are paid.

The NCC is part of Schedule 1 of the National Consumer Credit Protection Act of 2009. It is administered by the Australian Securities & Investments Commission (ASIC).

Mortgage delinquency rates may be stabilising, but as a mortgage professional, you can still do more to protect your clients. Among these is finding a lender that can offer them the best deal.

Our Best in Mortgage Special Reports page is the place to go if you’re looking for a lender that can provide a home loan that matches your clients’ needs. The companies featured in our special reports are vetted by our panel of experts as trusted and reliable market leaders. By partnering with these lenders, you can be sure that your clients are getting a mortgage that suits them.

What do you think about current mortgage delinquency rates in Australia? Does it paint a rosy picture of the country’s housing market? Feel free to share your thoughts below.